Fannie/Freddie Plaintiffs Realign Oral Argument: Hume on the Appeal, Barnes on the Cross-Appeal

Glen's Verdict

Plaintiffs stack their lineup by subject matter, not by client

Hume (Boies Schiller) argues the jury verdict; Barnes (Cooper & Kirk) argues the cross-appeal. Government doesn't object.

If you're new here: I'm Glen Bradford. I've been long Fannie Mae (FNMA) and Freddie Mac (FMCC) preferred shares for years. The full thesis — Net Worth Sweep">Net Worth Sweep, conservatorship, the math — is at glenbradford.com/fanniegate.

If you're back: Yesterday I wrote about the April 21 oral argument and the time allocation. One day later, the plaintiffs rewrote the lineup.

On April 14, 2026, Hamish Hume (Boies Schiller, counsel for the Class) and Brian Barnes (Cooper & Kirk, counsel for Berkley) filed a letter with the D.C. Circuit Clerk. The government doesn't object.

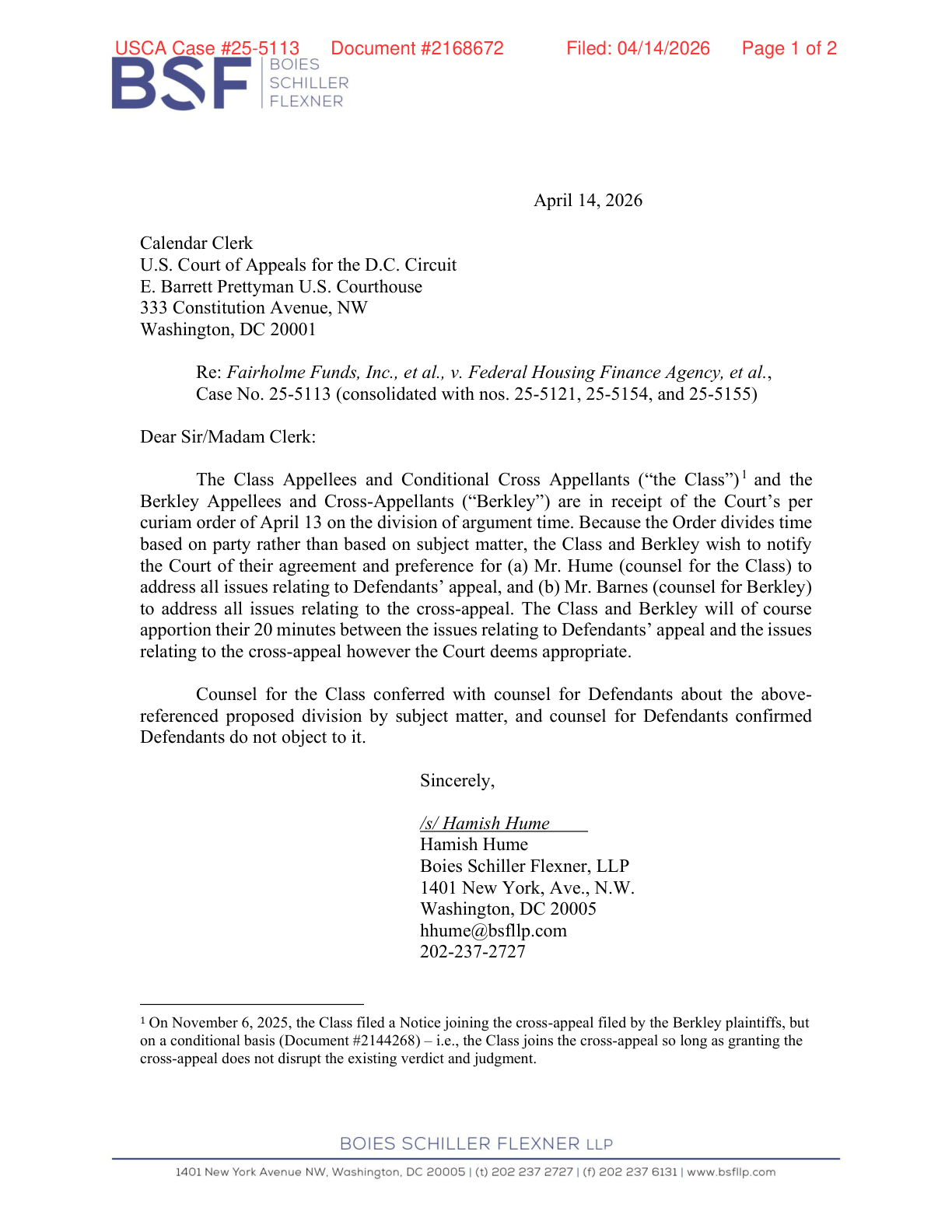

Here's the filing:

What Changed

The court's April 13 order divided oral argument time by party:

| Party | Time | |-------|------| | FHFA / Fannie / Freddie | 20 min | | Berkley Plaintiffs | 15 min | | Class Plaintiffs | 5 min |

The plaintiffs' letter asks the court to let them divide their combined 20 minutes by subject matter instead:

- Hume argues everything on defendants' appeal — i.e., defending the jury verdict.

- Barnes argues everything on the cross-appeal — i.e., the additional damages Berkley is asking the court to remand for.

The court still decides how to split the 20 minutes between the two topics. But one lawyer owns each topic.

Why This Is A Tell

Appellate argument is zero-sum. Every minute you spend switching context between your client's defense and your co-plaintiff's cross-appeal is a minute you don't spend answering the panel's hardest question.

Splitting by party is the default. It's what the court ordered. It's also not what two experienced appellate lawyers would choose if they were optimizing for outcome rather than client protocol.

Splitting by subject matter means:

- Hume — who ran the Class case and knows the verdict record cold — gets to defend it without having to also pivot to the cross-appeal damages theory.

- Barnes — Cooper & Kirk, the firm that has argued this constitutional/administrative-law turf at the highest levels — owns the cross-appeal, which is where the novel legal ask lives.

The plaintiff side put their best lawyer on each issue rather than each lawyer on their own client. That's what a coordinated appellate team does when it thinks it can win.

And the government agreed to it. Defendants had every right to object and force the party-based split. They didn't. Read into that whatever you like.

The Footnote Worth Reading

The letter's footnote is a quiet reminder of how tightly these two plaintiff groups are linked:

On November 6, 2025, the Class filed a Notice joining the cross-appeal filed by the Berkley plaintiffs, but on a conditional basis — i.e., the Class joins the cross-appeal so long as granting the cross-appeal does not disrupt the existing verdict and judgment.

The Class is backing the cross-appeal — but only to the extent it doesn't endanger what the jury already gave them. That's the entire plaintiff-side posture in one sentence: protect the verdict first, go for more second.

What I'm Watching On April 21

Same panel. Same 9:30 a.m. ET start. Same recording link: https://media.cadc.uscourts.gov/recordings/bydate/2026/4.

Now with a cleaner division of labor on the plaintiff side.

Go Deeper

- Yesterday's post — what the April 21 hearing is actually about

- The full Fanniegate thesis

- Fannie Mae preferred shares explained

- FNMA · FMCC

I hold long positions in Fannie Mae and Freddie Mac preferred shares. This post is my personal opinion and is not financial advice.

Free Tools & Calculators

Interactive tools built by Glen Bradford

Enjoyed this? Get more like it.

Glen's Musings — AI, investing, and building things. Occasional. Free.

Glen Bradford

Investor · Builder · Writer

MBA from Purdue. Former hedge fund manager. Holds 26 series of Fannie Mae and Freddie Mac junior preferred stock. Built Cloud Nimbus for Salesforce consulting. Author of Act As If. Writes about investing, building things, and the longest financial fraud in American history.

More in Fanniegate

Keep Exploring

FNMA Stock Forecast & Analysis

What actually drives Fannie Mae stock — catalysts, restructuring math, and honesty.

Read moreNEWGSE Catalyst Tracker

Track every signal toward Fannie & Freddie privatization

Read moreNEWFannie Mae Preferred Dividends

Every series, coupon rate, suspension status, and yield math if dividends resume.

Read moreNEWFannie Mae vs Freddie Mac

Side-by-side comparison — and why it doesn't matter for investors.

Read moreNEWBest Preferred Stocks to Buy

26 series Glen actually owns — with coupon rates, par values, and reasoning.

Read moreFanniegate Timeline & Evidence

The full timeline, 8 books, and the current status of recapitalization.

Read moreTrading Analysis — 4 Years of Data

Every trade, every ticker, every price. 2,068 transactions parsed and visualized.

Read moreHow to Buy Preferred Stock

Step-by-step guide from an investor who owns 26 series.

Read moreDisclaimer: This blog post reflects the author's personal opinions at the time of writing and is not financial, investment, or legal advice. Glen Bradford holds positions in securities discussed on this site. Past performance is not indicative of future results. Do your own research and consult qualified professionals before making investment decisions. Some content on this site was generated or edited with AI assistance.