The Fannie/Freddie Case Gets Oral Argument on April 21 — Here's What's at Stake

Glen's Verdict

April 21 oral argument is a meaningful catalyst

DC Circuit hears the Net Worth Sweep appeal — FHFA trying to overturn the jury verdict

If you're new here: I'm Glen Bradford. I've been long Fannie Mae and Freddie Mac preferred shares since before most people knew what the Net Worth Sweep">Net Worth Sweep was. I've written about this thesis for years at glenbradford.com/fanniegate — the history, the legal landscape, the preferred share structure, the math. If you found this post and you're not familiar with the case, start there. This post assumes you know the basics.

If you're back: April 21. This is the one.

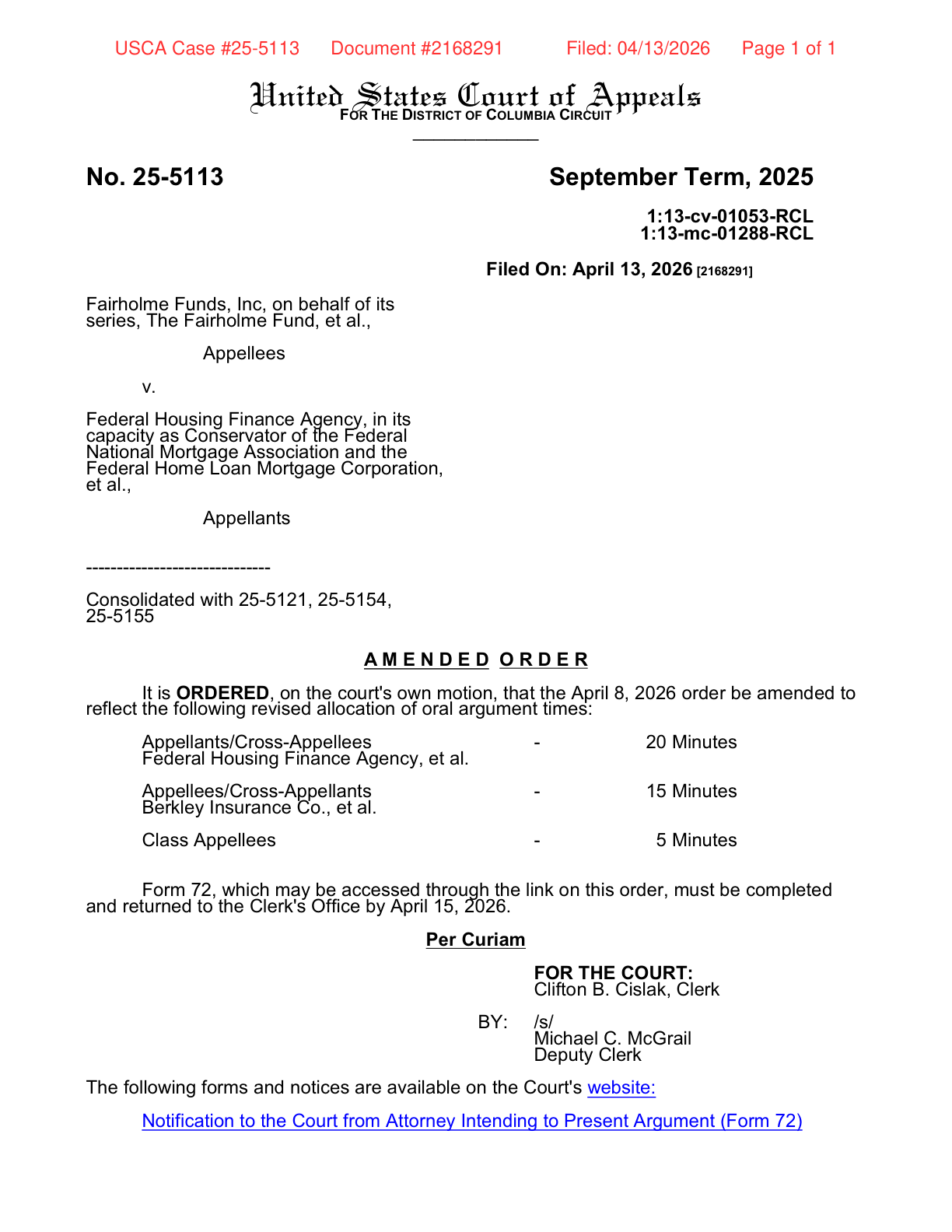

The D.C. Circuit just entered an amended order allocating oral argument time in the consolidated Fannie/Freddie class action. The hearing is set for Tuesday, April 21, 2026 at 9:30 a.m. before Judges Walker, Childs, and Ginsburg.

Here's the actual court order — filed April 13, 2026, Case No. 25-5113:

⬇ Download the full order (PDF)

The Time Allocation

Per the amended order:

| Party | Role | Time | |-------|------|------| | FHFA, Fannie Mae, Freddie Mac | Appellants / Cross-Appellees | 20 minutes | | Berkley Insurance Co., et al. | Appellees / Cross-Appellants | 15 minutes | | Class Appellees | Appellees | 5 minutes |

The underlying case numbers: 1:13-cv-01053-RCL and 1:13-mc-01288-RCL before Judge Lamberth, consolidated with 25-5121, 25-5154, and 25-5155 at the D.C. Circuit level.

Who Is Who

FHFA (Appellants) — The Federal Housing Finance Agency, acting as conservator of Fannie Mae (FNMA) and Freddie Mac (FMCC), is the one appealing. They want the D.C. Circuit to throw out the jury verdict. They get 20 minutes.

Berkley Insurance Co. (Appellees/Cross-Appellants) — These are the shareholder plaintiffs who won at trial. They're defending the verdict and cross-appealing — asking the court to go further and remand for an additional trial on damages not covered in prior proceedings. They get 15 minutes.

Class Appellees — The broader class of shareholders, also defending the jury verdict. 5 minutes.

Fairholme Funds (Bruce Berkowitz) — Named as an Appellee in the caption. Defending on the merits.

Everyone on the plaintiff side is trying to hold onto what the jury gave them. FHFA is trying to take it back.

What This Case Is About

The Net Worth Sweep.

In 2012, FHFA amended its conservatorship agreements with Fannie and Freddie to direct 100% of their profits to the Treasury in perpetuity — eliminating any possibility that shareholders would ever receive a return. No dividends, no path to recap, no end in sight.

The plaintiffs argued this went far beyond what a conservatorship is legally permitted to do. A conservatorship is supposed to stabilize and return a company to health — not extract every dollar forever. They argued it amounted to an unlawful taking.

A jury agreed. A jury said the government did something it wasn't allowed to do.

FHFA is now asking the D.C. Circuit to throw that verdict out.

The appellate question: was the jury right? And should Berkley get additional damages on top of what was already decided?

Why April 21 Matters

Oral argument isn't a second trial. The judges have read every brief. Argument is their chance to press both sides on the weakest parts of their positions — and the questions they ask are often the most useful signal of where the panel is leaning.

The allocation itself is interesting. FHFA gets 20 minutes. The plaintiffs collectively get 20 (15 + 5). Equal time. Nothing is predetermined, but equal time isn't what you give a hopeless appeal.

The panel composition matters too. Judge Justin Walker has been vocal about administrative agency overreach — post-Chevron overrule, that skepticism has teeth. Senior Judge Douglas Ginsburg (not Ruth Bader Ginsburg — this is the other one, a Reagan appointee with decades on the D.C. Circuit) brings a long record on administrative law. Judge Childs is newer. Any of them can write the opinion that moves this.

The Recording

The D.C. Circuit posts recordings the same day arguments conclude.

April 21, after 9:30 a.m. ET: https://media.cadc.uscourts.gov/recordings/bydate/2026/4

I'll be listening live. Worth your time if you hold preferred shares.

My Position

I've been long Fannie Mae and Freddie Mac preferred shares for years. The full thesis — the history of the conservatorship, the Net Worth Sweep, the legal battles, the preferred share structure, the math on what a recap would mean — is all at glenbradford.com/fanniegate.

The short version: the GSEs were placed into conservatorship in 2008 to stabilize them during the financial crisis. They stabilized. Fast. They've since returned over $300 billion to Treasury — far more than was ever extended to them. The Net Worth Sweep wasn't part of the original deal. It was added in 2012 when the GSEs started becoming profitable again, apparently to prevent that profit from flowing back to shareholders.

A conservatorship preserves and returns an entity to health. It doesn't harvest it indefinitely.

The legal question has never gone away. Courts have been slow. Politics have shifted. Administrations have come and gone. But the underlying facts haven't changed, and neither has the legal argument.

April 21 is a big day.

If You Want to Go Deeper

- Full Fanniegate thesis — the whole story

- Fannie Mae preferred shares explained — what you're actually buying

- FNMAS preferred dividend calculator — model the scenarios

- FNMA stock profile — Fannie Mae common

- FMCC stock profile — Freddie Mac common

- Tim Pagliara — Investors Unite, the shareholder advocacy org that's been fighting this longer than anyone

I hold long positions in Fannie Mae and Freddie Mac preferred shares. I have for years. This post is my personal opinion and is not financial advice. Do your own research. The full thesis is at glenbradford.com/fanniegate.

Free Tools & Calculators

Interactive tools built by Glen Bradford

Enjoyed this? Get more like it.

Glen's Musings — AI, investing, and building things. Occasional. Free.

Glen Bradford

Investor · Builder · Writer

MBA from Purdue. Former hedge fund manager. Holds 26 series of Fannie Mae and Freddie Mac junior preferred stock. Built Cloud Nimbus for Salesforce consulting. Author of Act As If. Writes about investing, building things, and the longest financial fraud in American history.

More in Fanniegate

Keep Exploring

FNMA Stock Forecast & Analysis

What actually drives Fannie Mae stock — catalysts, restructuring math, and honesty.

Read moreNEWGSE Catalyst Tracker

Track every signal toward Fannie & Freddie privatization

Read moreNEWFannie Mae Preferred Dividends

Every series, coupon rate, suspension status, and yield math if dividends resume.

Read moreNEWFannie Mae vs Freddie Mac

Side-by-side comparison — and why it doesn't matter for investors.

Read moreNEWBest Preferred Stocks to Buy

26 series Glen actually owns — with coupon rates, par values, and reasoning.

Read moreFanniegate Timeline & Evidence

The full timeline, 8 books, and the current status of recapitalization.

Read moreTrading Analysis — 4 Years of Data

Every trade, every ticker, every price. 2,068 transactions parsed and visualized.

Read moreHow to Buy Preferred Stock

Step-by-step guide from an investor who owns 26 series.

Read moreDisclaimer: This blog post reflects the author's personal opinions at the time of writing and is not financial, investment, or legal advice. Glen Bradford holds positions in securities discussed on this site. Past performance is not indicative of future results. Do your own research and consult qualified professionals before making investment decisions. Some content on this site was generated or edited with AI assistance.