10 Best Chinese Microcaps

By Glen Bradford

Hi, I’m Glen Bradford. I was only trading my college tuition. As of today I am also trading my roommate’s college tuition. I wrote for TheStreet.com last fall and undertook equivalently 25 Credit Hours of MBA courses at Purdue University. I’m currently in the top 1% of Motley Fool CAPS players. For those of you that want to join me and make something out of nothing, I’m going to introduce you to the most ridiculously undervalued Chinese Companies on the face of the planet.

The requirements for these companies:

1. High Growth.

2. Profitable.

3. Selling less than Book Value.

4. Cheap based on Earnings (incl. Positive Cash Flow From Operations).

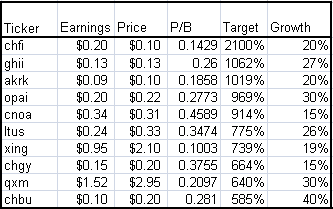

I’ll start with the top and work down. The Target value is a calculation composed of 3 parts: 1/3 Book Value + 1/3 P/E of 8 + 1/3 P/E of Growth. I have adjusted some of these numbers to remove 1-time expenditures, the potential of share dilution, intangible equity, etc. To be honest, all of these stocks should trade much higher than their target. This just helps me price companies in the midst of a crisis.

1. China Finance (CHFI) was sold down 50% on record breaking volume Monday while I was backing up the truck of bullishness. China Finance is responsible for helping small to medium Chinese enterprises go public in the United States. What makes this case unusual is China Finance’s assets are highly liquid — they could sell them in the market at the current price. Monday, their largest position Jade Art was unchanged, 2nd largest position Gulf Resources was up 8.3%, 3rd largest China Organic Agriculture (also covered in this article) was up 6.9% on higher volume. It’s not surprising that a company responsible for taking podunk Chinese companies public struggled through 2008. My estimates on this stock put it in 100-bagger territory from its 52-week low of $0.04. China Finance also helped two other of my picks — China 3C Group (CHCG) and Oriental Paper (OPAI). At $0.10, China Finance is selling at less than it’s highly liquid securities, especially after you take into account their price appreciations since December 31, 2008.

2. Gold Horse International (GHII) ran 44.44% Monday on above average volume. An Investor Village page was put up this weekend and had over 300 visitors in the first 24 hours. Not bad for a Chinese Wind Power play that’s profitable and has a P/E under 1 and is selling at 26% of Book Value. Their forecast for 2009 is 30% growth. That was before they announced they are headed to NYC to raise capital for even more growth!

3. Asia Cork (AKRK) manufactures “green” building materials in China. I took the liberty of visiting several local flooring and roofing places like Ocean Seven Roofing here at Purdue and confirmed that Cork Flooring is in high demand and is durable. Asia Cork is thinly traded at $3.57M, but at a P/E of 1 when it grew last year by 30% and is adding to production capacity leading into 2009.

4. Oriental Paper (OPAI), as mentioned earlier under China Finance, is growing 30% a year by manufacturing and distributing paper and paper products in China. Cramer recently indicated that things are looking good in the world of Corrugated Paper. This makes Oriental Paper is look even better.

5. China Organic Agriculture (CNOA) bought the Bellisimo Vineyard in California for about $14M and is trading at $23M. Compare this to their revenues in 2008 at $112M. Granted, they paid to much for Bellismo if you are looking at present discounted cash flows. When you look at the value of a California Wine label in China where China Organic distributes the stuff, you begin to see the big picture profit potential.

6. Lotus Pharmaceuticals (LTUS) just ditched their part time CFO Adam Wasserman (who still works for Gold Horse). Management forecasts growth between 30% to 40% and has so much in the pipeline and in progress for a $14.1M company that it’s ridiculous.

7, 8. Qiao Xing Universal Telephone (XING) is trading at $65M. Qiao Xing Mobile Communication (QXM) is trading at $140M. Seeing as how I already like QXM, and how XING owns 70%+ of QXM, shouldn’t XING be valued at least at $100M?

7.

8.

9. China Energy Corp (CHGY) is enormously undervalued when you take into account the various reasons they have been unable to produce at maximum capacity, for example — the expansion of capacity by 60%, the Olympic Games, and most recently the increase in safety standards. They produce and process raw coal for heating and power generation in Inner Mongolia. My earnings estimates are adjusted to reflect what I’d consider to be normal operating conditions.

10. China Agri-Business (CHBU) is probably one that I shouldn’t tell you about. I keep buying it at around $0.21 and selling at $0.40 (on a daily basis). Remember, that secret cash loop that only exists in video games that you wished existed in real life? This is it. Right now the entire company is priced at $2.59M. Their latest reported cash balance is $8.3M and their liabilities are $561M. Yes — they are selling at less than half of net cash (cash – total liabilities). But, now that you know I can say bye-bye to my infinite money loop.

I’m the kind of guy that questions everything and is willing to take a stand until empirically proven otherwise. So far, my allocation decisions empirically prove that I know what I’m doing — so much for that efficient market hypothesis.

Disclosure: Glen and his investors own chfi, ghii, akrk, opai, cnoa, ltus, xing, chgy, qxm (through xing), chbu, chcg.