2 Articles and my radar

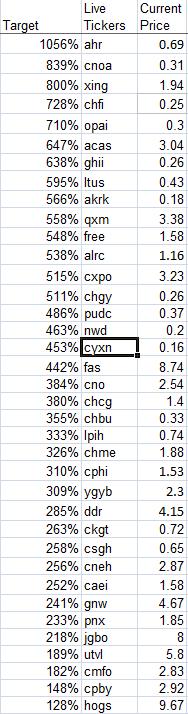

Anthracite Capital is Reinflating By Glen Bradford Instead of talking about finance institutions that are being diluted like Citigroup (C) and financial institutions that are so hot they’re already above their November lows like Wells Fargo (WFC) and Goldman Sachs (GS), I’m going to introduce you to a better place where it’s bottoms up from here. After getting the wind knocked out of it, Anthracite Capital shows signs of life. Granted that the price has probably exploded higher from $0.74 by the time this article gets published, let us use it at a baseline. What do we know about Anthracite at $0.74?

- Anthracite is trading at a P/E of 0.487 if you knock out the Q4 2008 earnings nightmare and look back 1 year from Q3. The reason I took out Q4 is because the loss claimed appears to be a one-time huge write off, followed by positive earnings the next quarter.

- Anthracite Capital is trading at a book value of 0.1.

- Anthracite Capital is traded on the New York Stock Exchange. Let me repeat. This is a company cheaper than the listing requirements on the New York Stock Exchange. It either increases in price or eventually gets delisted. All of these figures indicate that Anthracite is priced for bankruptcy. Where’s the good news?

- They have pushed back the disaster twice already and have been in talks to resolve the issue. If I know anything about creditors, the last thing they want to do is run their debtors into the ground.

- Anthracite was profitable in Q1 2009, just not as profitable as it used to be. If you optimistically flat line the profit figures from Q1 2009 into the future, your P/E is still 0.685. Note that Q1 of 2008’s Net Income Applicable to Common Shareholders is twice as large of that of any quarter as far back as I can see. So, comparing Q1 2009 to Q1 2008 isn’t fair to begin with. The bottom line here is that comparing the income of Q1 2009 to Anthracite’s history --- things match up but the revenues are weaker. So, what am I doing about it? I’m buying. I probably already have a sizeable position. I’d say you could add this to my suggestions for 100% in 1 month, but that would be an understatement. I’d be surprised if AHR didn’t see $2 by June 18th. Disclosure: Glen and his investors own AHR.

Title ideas: China: Harder, Better, Faster, Smaller China: Go Small Or Go Home By Glen Bradford Cramer’s a buyer of Bucyrus. I’ve been a fan of Bucyrus since I came across it in late August 2008. Back then, I grabbed the coattails of the top of the roller coaster and rode it down from $67 to $62. If I liked it then, imagine how much I like it now at $23, on its way back up. Up over 100% from its low, why is this growing company trading so cheaply with a P/E of 6.86? I’ve got one idea. Opportunity cost. If you want to play china the right way right now, you have to start small and work your way up to see the big picture. Bucyrus makes the mining equipment. Let’s take a look at some folks that may use this kind of equipment and are trading at a discount to Bucyrus. To set the stage, Bucyrus has a P/E of 6.8 and is selling at 1.7x Book Value. Let’s look at some undervalued Oil and Coal ideas that are all less than half as expensive as Bucyrus with respect to both metrics.

- Puda Coal (PUDC) is being featured at the China Rising Investment Conference today and is set to run from 10:00-10:30am. Puda Coal is a supplier of metallurgical coking coal to the industrial sector in the PRC. They are currently in the process of vertically integrating their supply chain. Goldman Sachs just upgraded the entire coal industry. The reason for upgrading the industry is mostly due to China. Looking at these numbers, I’m going to agree with Goldman.

- Longwei Petroleum Investment Holdings (LPIH) is one of the leading diesel, gasoline, fuel oil and solvent oil distributors/wholesalers in Taiyuan City, Shanxi Province, P.R. China. Do note that they’re expansion is being financed through their working capital. Bank loans in China have been unbearably tough to get this last year --- so this is a strong point.

- China North East Petroleum (CNEH) is engaged in the exploration and production of crude oil in Northern China. They just signed a contract to drill another 48 wells in the next 10 months, taking their total to 303 after the project is completed. Crunch the numbers and that’s 18% growth in production in 10 months.

- Now, I would outline the advantages of China Energy (CHGY), but I did that 2 weeks ago. Instead I’ll give you a bonus pick that’s American. Crimson Exploration (CXPO) is even less than half of half as expensive by both metrics as Bucyrus. They are an independent natural gas and crude oil company engaged primarily in the United States, Gulf Coast and South Texas regions. Now, I’m not telling you that you’re not likely to make a lot of money on Bucyrus right now. What I’m saying is that if you have two opportunities, and one of them is more likely to return more money than the other --- it would make sense to buy into the one with better returns, right? That said, Bucyrus in my opinion is definitely worth more in the long run. It’s trading less than its backlog and that’s pretty much sinful. Disclaimer: Glen and his investors own LPIH, PUDC, CNEH, CHGY, CXPO.

Free Tools & Calculators

Interactive tools built by Glen Bradford

Enjoyed this? Get more like it.

Glen's Musings — AI, investing, and building things. Occasional. Free.

Glen Bradford

Investor · Builder · Writer

MBA from Purdue. Former hedge fund manager. Holds 26 series of Fannie Mae and Freddie Mac junior preferred stock. Built Cloud Nimbus for Salesforce consulting. Author of Act As If. Writes about investing, building things, and the longest financial fraud in American history.

More in Life & Philosophy

Keep Exploring

Net Worth Percentile Calculator

Where do you rank financially? Find out instantly.

Read moreAct As If — Glen's Book

Talk minus action equals zero. The philosophy that drives everything.

Read moreGlen's Rules

The principles behind the investing, the building, and the writing.

Read moreAll Life & Philosophy Posts

Browse the full Life & Philosophy blog archive.

Read moreDisclaimer: This blog post reflects the author's personal opinions at the time of writing and is not financial, investment, or legal advice. Glen Bradford holds positions in securities discussed on this site. Past performance is not indicative of future results. Do your own research and consult qualified professionals before making investment decisions. Some content on this site was generated or edited with AI assistance.